By Dex / August 21, 2025

The healthcare system in the Philippines, especially PhilHealth, is sadly unreliable. With corruption and inefficiency in the government, I can’t help but worry that by the time I retire, PhilHealth might not even exist anymore. And even now, its coverage is so limited that it can’t fully pay for even simple illnesses—what more if it’s a major hospitalization? Would you really entrust your health and future to the government? Definitely not.

That’s why I took action early and availed Kaiser’s long-term 3-in-1 healthcare plan. It gives me confidence knowing I have not only healthcare protection today, but also savings and investment that will benefit me and my family in the future.

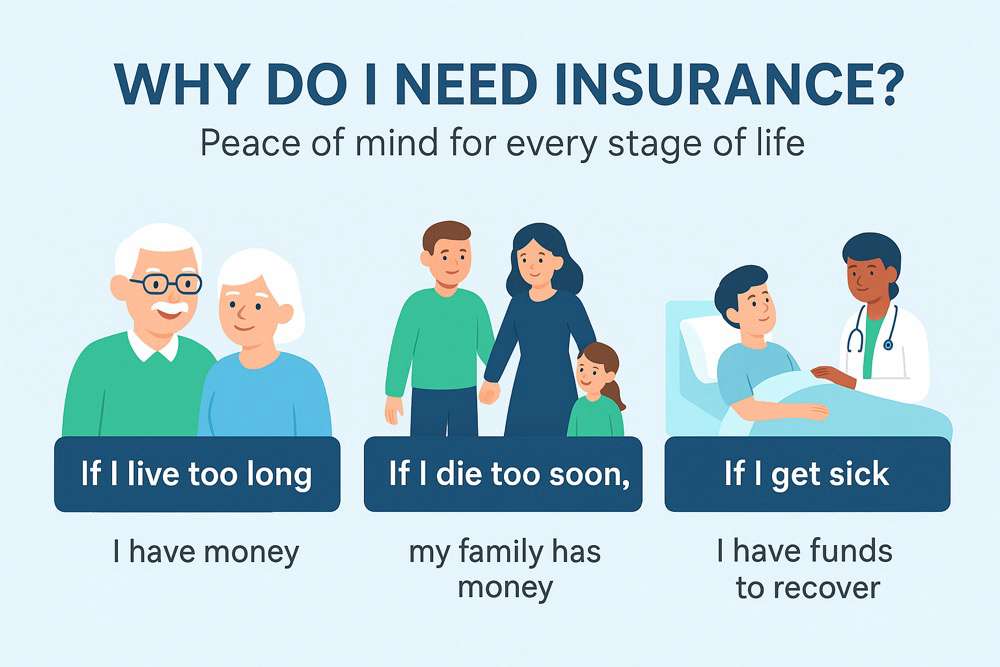

We all know that getting sick is expensive. A short hospital stay can already cost tens of thousands of pesos, and for serious illnesses, bills can climb to hundreds of thousands or even millions. Relying only on PhilHealth or on personal savings is risky, because one medical emergency can wipe out everything you’ve worked hard for. This is why having private healthcare coverage is no longer a luxury—it’s a necessity.

Kaiser is a trusted Health Maintenance Organization (HMO) in the Philippines that offers something unique compared to traditional HMOs. It combines healthcare, savings, and investment in one program, which is why it’s called a 3-in-1 product. Instead of just giving you health coverage for a year, Kaiser also builds up funds you can use in the future.

1. Healthcare – Provides hospitalization benefits, annual check-ups, and access to a wide network of hospitals and doctors nationwide.

2. Savings – A portion of your payment is set aside and grows over time.

3. Investment – Your money is invested, allowing it to earn returns and give you long-term financial growth.

The best part? Even if you don’t get hospitalized, your money isn’t wasted—it continues to grow and work for you.

• Affordable premiums compared to paying hospital bills out of pocket.

• Cashless hospitalization in accredited hospitals and clinics.

• Wide network of doctors and hospitals in the Philippines and abroad.

• Long-term growth since your plan doubles as savings and investment.

• Lifetime healthcare after completing the program—perfect for retirement.

• Young professionals who want to start early with both healthcare and financial planning.

• Parents who want protection and a financial cushion for their families.

• OFWs who want peace of mind for their loved ones back home.

• Retirees who no longer have company healthcare benefits but still need reliable coverage.

Most HMOs follow a “use it or lose it” system—if you don’t get sick, your money is gone. Kaiser, on the other hand, is different. If you don’t use your health benefits, your money continues to grow as savings and investment. It’s protection and wealth-building combined.

• A family with Kaiser didn’t need to worry about hospital bills that reached hundreds of thousands because their plan covered it.

• A Kaiser member who stayed healthy still enjoyed the returns on their plan after maturity, giving them a retirement fund they could use freely.

• Reach out to a licensed Kaiser financial advisor or agent.

• Choose the plan that best fits your budget and needs.

• Pay monthly, quarterly, or annually depending on what’s convenient for you.

• Enjoy the peace of mind knowing that you’re covered for both today and tomorrow.

Health is wealth—but in the Philippines, healthcare can be a financial burden if you’re not prepared. Relying only on PhilHealth is not enough. That’s why I chose Kaiser’s long-term 3-in-1 healthcare plan. It gives me the security of healthcare today, the growth of savings, and the power of investment for the future.

If you want real protection and financial peace of mind, don’t wait until it’s too late. Take charge of your health and future with Kaiser.

Seafarer and Family Man

I'm Dexter— a seafarer by profession, a traveler by passion, and a homebody by choice.

Leave A Comment